NYC Real Estate Buyers and Sellers Breathe Easier as L Train Shutdown Called Off

As reported by the New York Times, Governer Cuomo has called off a planned shutdown of the L subway track, which would have lasted 15 months. The shutdown, which was intended to repair structural damage caused by Hurricane Sandy in 2012, will be replaced by a program of gradual repairs, and will accommodate full weekday service with some partial weekend closures.

The cancellation of the long-awaited (and dreaded) track closure is a cause for cautious celebration in neighborhoods such as Greenpoint and Williamsburg in Brooklyn, which rely on the L train for convenient access to and from Manhattan. While the future of the track will be fully revealed in time, as work continues assess and repair the remaining structural damage, the new plan is likely to be a boon to those looking to buy or sell near the L train’s route.

Westchester NY Real Estate Attorneys Beware: Fair Housing Law Amended to Protect Co-Op Purchasers

In an effort to combat discriminatory practices by coop boards, Legislators in Westchester have amended the county’s Fair Housing Law (Article II of Chapter 700), effective immediately.

This new amendment attempts to close a loophole by which coop boards could potentially discriminate against prospective purchasers by delaying action on their application beyond a reasonable time frame, or by failing to notify an applicant if their application was incomplete, rather than rejecting them outright.

Upon receipt of an application, coop boards must now inform the applicant within fifteen days as to whether the application is complete or incomplete. If incomplete, the same time frame applies to the re-submitted application.

In addition, the board now must provide a written notice of acceptance or rejection to the applicant within sixty days after receipt of a completed application. If rejected, a copy of the notice must be sent to the Human Rights Commission no more than fifteen days after it has been sent to the applicant.

The new law, which has been decades in the making according to County Executive George Latimer, has not yet been taken up outside of Westchester County, though it is possible that such a measure may be discussed in the future. For more info, please see the full text of the law here.

The Top 5: What Bankers Love to See From Their NYC Real Estate Attorney

Our firm has represented a multitude of lenders in NYC real estate transactions over the years, working closely with loan officers and borrowers to see all parties to a smooth and successful closing.

While each lender works somewhat differently, our experience has given us significant insight into what bankers love to see from their attorneys. From conversations with the loan officers we represent, we have compiled a list of “best practices” below, which we hope will help bank attorneys provide the best level of service to their clients.

Without further ado, here are our top five tips!

- Proactive Weekly Updates:

No matter how many files are assigned to a specific bank attorney, it is helpful to the loan officer to provide an update once a week on the status of all of their open files. By providing this, the loan officer and bank attorney can ensure they are on the same page. Often, this will force further updates which help keep the rest of the team informed.

- Invitation to the Closing:

Many loan officers have expressed to us that they like receiving a calendar invite with the date, time, and location of the closing once it is scheduled. This way, they have the information readily available if they are traveling to the closing, or their client asks them to confirm it, or if they are simply having a hectic day.

- Aztech Package Delivery:

If a transaction is for a co-op, and the lender requires the bank attorney to draft and send the Aztech forms to the client, a quick email to let the loan officer know (as well as the buyer’s attorney if the transaction is a purchase) can go a long way to avoiding any potential delays. The address that the package was sent to and the tracking information should both be included. This way, everyone can make sure that the clients receive the forms, as unfortunately packages can sometimes be lost, stolen, or not delivered.

- Keeping Connected:

With so many people working together on a transaction, from loan officers to processors and underwriters to the bank attorney, it often happens that someone is not included on an important email. The bank attorney can help by being aware of this, and adding anyone who was excluded to the chain. It is best to keep the entire ‘team’ on every email—even if a particular email does not immediately pertain to everyone, it may hold information that is relevant to them later in the process.

- The Post-Closing Check-In:

Sometimes a loan officer is not able to be present at a closing. In these cases, we find that they appreciate an email afterward advising that the closing is complete, along well as any ‘color’ or ‘play by play’ as to what happened at the closing table. This information helps the loan officer prepare to follow up with their client afterward, particularly if any issues occurred during the signing process.

By now, you’ll have noticed that all of these tips share a common theme: communication! Being proactive and keeping your client updated at every point in the process is a tried and true way to provide the best possible service.

Did we miss anything in our list? Let us know! We’d love to hear your suggestions.

I Bought a Condo in NYC—Do I Need to Pay for my Recorded Deed?

This is one question that we hear frequently from our former clients, and the short answer is — no.

Once closing is complete, the title company is responsible for ensuring that the deed becomes public record by sending it to the county clerk for recording. Once the deed is recorded, the county clerk’s office generally mails the deed to the Purchaser’s attorney. Receipt of the original, recorded deed prompts our office to check the online records for further verification. We then send a copy of the deed to the client for free, as part of their final closing package.

New condo and house owners may receive official-looking letters advising them to pay for their original deeds. The letters offer to have the recorded deeds printed and sent to the new homeowners for a fee. These letters can look eerily like official government correspondence, but – as our savvy blog readers will know – they are not.

The important thing for NY condo and house owners to remember is that, even if they lose their copy of the deed, the deed is a public record. For New York City residents at least, recorded documents can be accessed any time for free through the Automated City Register Information System (ACRIS).

If you have further questions about how to access your deed, or about unusual correspondence received after closing, feel free to reach out to us.

Updated FinCEN Geographic Targeting Orders and Their Impact on NYC Real Estate Transactions

The Financial Crimes Enforcement Network (FinCEN), a division of the US Treasury Department, will again extend the Geographic Targeting Order (GTO) which first went into effect in 2016. This extension will last from November 16, 2018 to May 15, 2019.

The GTO’s purpose is to combat money laundering schemes by identifying individuals behind companies and other entities purchasing real estate. To qualify for reporting under the GTO, a transaction must meet four criteria:

- The property being purchased must be in an area covered by the GTO. In New York, this includes all of New York City’s five boroughs. However, certain counties in Texas, Florida, California, Hawaii, Nevada, Washington, Massachusetts, and Illinois also apply.

- The buyer is a Legal Entity, such as a limited liability company or partnership. It should be noted that, as of the new extension, Trusts are no longer defined as a Legal Entity for the purposes of the GTO.

- The consideration is greater than $300,000.00.

- The purchase price is not paid using any external financing from a financial institution, and is being paid in any part with cash, certified check, personal check, traveler’s check, attorney escrow check, money order, wire transfer, or e-currency.

Any transaction meeting the above criteria must be reported to FinCEN within 30 days of closing.

For more details, you can find the FinCEN website here.

GUEST BLOG: How Lenders and Banks Approve Coops and Condos for NYC Apartment Purchases

By Keith Furer, Guardhill Financial

Be a smarter investor by understanding how lender approvals on buildings work.

Whenever someone gets a mortgage on a unit within a coop or condo, a lender must not only approve the borrower, but separately approve the building. Like the borrower, a coop or condo must also meet certain requirements in order for a lender to place a mortgage on a building unit.

Specific lender requirements on buildings vary not only between lenders themselves, but also between condos and coops.

Examples of Lender Requirements on Coop and Condos:

– stable financial standing

– acceptable owner occupancy rates

– valid and up-to-date building insurance

– maximum commercial square footage

– absence of major litigation

But what’s actually involved in the approval process of a coop and condo by a lender?

Sometimes a lot, and sometimes very little.

To help demystify the process, the following are the main steps typically carried out by a mortgage professional like myself:

1. Check the Systems, Get Management Contact Info

My first step is to do a check of the building address in various online systems to see if the project has been approved or declined in the past by any lenders. Depending on how up-to-date the information is, that could determine whether it is wise to proceed with the purchase or not.

If a coop or condo shows up as approved with most lenders, including recently updated financial information, etc., that may be all the information that’s needed, depending on which lender will make the mortgage. However, this is rare, as there is usually at least one supporting document in need of updating.

The contact information of the building’s management is always required, regardless of whether it is professionally managed or self-managed. The real estate agent representing the property and your attorney will typically have this information. Most management companies today charge at least a nominal fee for coop and condo documents.

2. Getting & Submitting the Core Information

Assuming a coop or condo needs updated documents, my team will then contact the management entity to get the standard information, including two years financials, a building questionnaire, and underlying project insurance. These can offer a fairly complete picture of a building’s status, but sometimes other documents are required, like a recent budget and offering plan.

The financials show the overall financial health of a condo or coop, the budgeting, the reserves, etc. Two years are required so a building can demonstrate a more complete snapshot of its most recent results.

The coop or condo questionnaire contains all the basic information about the building, including everything from information on occupancy levels to initial sponsor information, to the underlying mortgage, and much more. The questionnaires typically run two to three pages.

Once we have the required documents, my team submits them to the applicable underwriting department along with the borrower documents. Quite often we are able to have the project approved or re-approved prior to the buyer signing the contract.

3. Proactive & Precision Follow-up Required

Whenever anyone gets a mortgage on any type of property, there are a lot of moving parts that have to be in place in a timely manner for that mortgage to close. My team and I move quickly across all the channels of the process, particularly when it comes to coop and condo approvals.

It is vital to be proactive with these approvals, because in some cases, they can drag out, and that can push back closing dates, which nobody likes or wants. Whether it’s coop or condo documents that are in the midst of being updated, or extended turnaround times for receiving documents, I’ve witnessed a lot of unforeseen delays.

In the cases when we come across any potential red flags for a coop or condo, like low occupancy rates or upcoming assessments, we communicate them with our clients and their attorneys and address each one head-on with the underwriters. Just because there’s a red flag doesn’t necessarily mean that there’s a problem, it just means there’s a matter to be resolved. The earlier red flags are identified and addressed, the smoother the whole process goes, and increases the likelihood of closing without delay.

Sometimes the coop and condo approval processes can be quick and sometimes they can drag on. Make sure you have the right team working for you to be proactive and help insure that you close on time.

Guest blog entries are for the benefit of the real estate community and do not necessarily reflect the views of this law firm.

Deadlines Within Deadlines: Cooperative Board Packages and Commitment Letters in NYC Real Estate Closings

A buyer (for purposes of this article, let’s call her Sally Streetwise) works with her broker to find a property she loves in a beautiful cooperative. The brokers work with the buyer and the seller to reach agreement on the key deal points and then turn the delicate deal over to the lawyers to conduct due diligence and to negotiate the more formal contract terms. After much back and forth between lawyers and clients, the contract is finalized, the buyer signs the contract and submits her deposit check, the seller’s attorney deposits the check to an escrow account, and the contract is fully executed.

You might think this would be a great point in time for the brokers, lawyers, buyers and sellers to take a collective sigh of relief, pat themselves on the backs, and look forward to a smooth closing. Alas, there is no rest for the weary in Manhattan real estate. With the finalization of the contract comes something lawyers and brokers deal with every day of their careers, but something first-time buyers like Sally Streetwise may not yet be fully prepared: DEADLINES, and the pitfalls for missing them.

The New York residential real estate contract will not satisfy itself with simply one deadline. There must be multiple deadlines, as many deadlines as there are subway lines (or double-parked cars) in Manhattan: Deadlines to apply for mortgages. Deadlines to obtain Commitment Letters. Deadlines to submit board packages. Deadlines for providing notices. Deadlines to schedule closings. Deadlines to adjourn closings. Deadlines that increase stress and confuse everyone throughout the process. While some lawyers, bankers, and brokers push forward as quickly as possible hoping that they avoid any deadline land mines, experienced practitioners will help the buyer navigate deadlines to lessen their stress and protect their best interests.

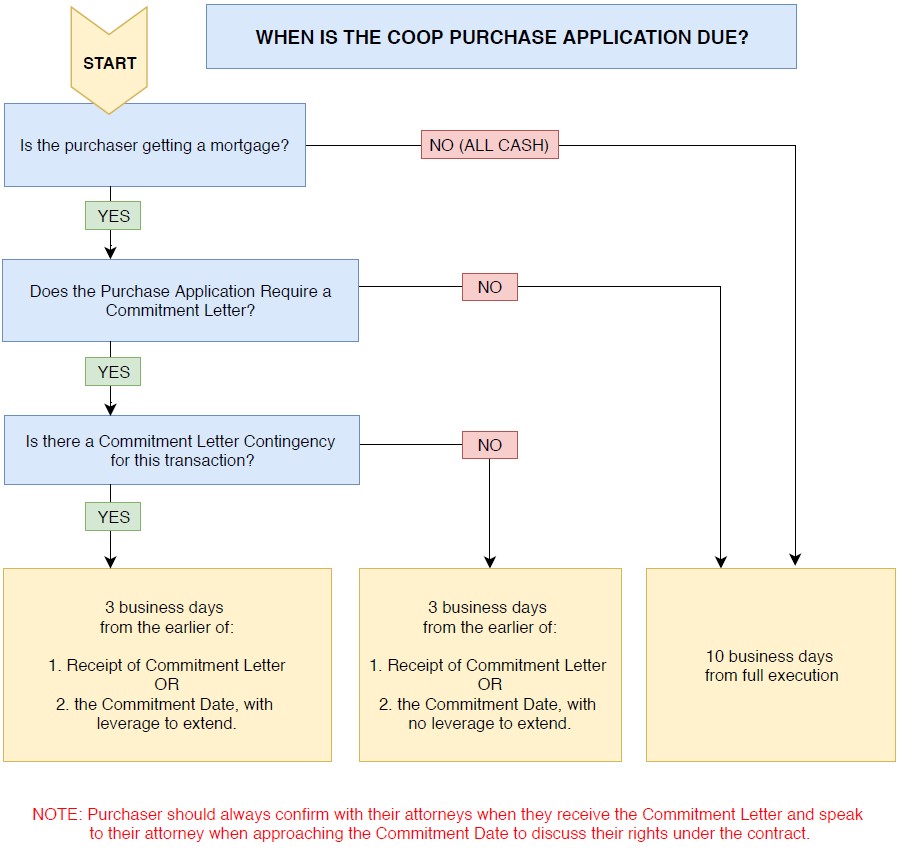

Let’s spend a few minutes to get acquainted with two of the most significant deadlines our buyer will encounter once she gets into contract: the board package submission deadline and the loan Commitment Letter deadline (“Commitment Date”). In the typical contract for the purchase of a cooperative unit, the answer is clear: Sally Streetwise has ten business days to submit her board package. Unless she has three business days. But remember that the three-business-day deadline begins to run at the expiration of a completely different thirty or forty-five-calendar-day Commitment Date. Sometimes. Or it begins to run sooner.

Let’s break that down a little bit further to clear up this confusion. One commonly used contract contains multiple deadlines for the submission of the board package, depending on different circumstances that might exist:

If Sally Streetwise is not seeking financing, and is proceeding “all cash,” she will need to submit her board package within ten business days of her attorney’s receipt of a fully executed contract (unless otherwise negotiated).

If Sally is seeking financing, then the determining factor for the board package deadline will be whether a commitment letter is required to be submitted with her board package. If the board does not require a commitment letter as part of the board package, then the original ten-business-day deadline is still in effect. However, most boards do require a commitment letter because most boards reasonably believe that if a buyer is unable to obtain a commitment letter, the deal will not go forward. There would be no point wasting time reviewing such an application.

If the board requires a commitment letter as part of the board package, then it’s important to note that the contract will include the Commitment Date of usually thirty or forty-five days from the date Sally’s attorney receives a fully executed contract. Sally’s board package deadline also then hinges on whether her contract has a Commitment Letter contingency.

If Sally’s contract has a Commitment Letter contingency, then her deadline is three business days from the earlier of when she receives the Commitment Letter or the Commitment Date.

If, on the other hand, Sally is seeking financing but her transaction does not include a Commitment Letter contingency, then Sally’s deadline is three business days from the earlier of: (1) when she receives the Commitment Letter or (2) the Commitment Date, with one important caveat: even if Sally has not obtained a Commitment Letter by the Commitment Date, she must still submit her board package within three business days from the Commitment Date.

Given the complexity described above, we would always recommend that a potential buyer, with the assistance of her broker, obtain a copy of the board application before entering into the contract for the purchase of the cooperative unit. This way they will know ahead of time whether the board requires the commitment letter as part of the board package and thus the deadline to submit that package. The broker and the buyer should work together to get the board package as complete as possible so that the only open item remaining while approaching the Commitment Date will be the lender’s issuance of a Commitment Letter.

One common pitfall to note: we all come across deadlines in our daily lives. When facing a deadline, there’s often an impulse to hurry up and beat the deadline by as many days as you can. In the context of the Commitment Date described above, and board package deadline, however, this is not necessarily the best path forward.

Once parties are in contract, Sally Streetwise should start working on her loan with her banker and on the board package with her broker. The goal for both is not necessarily to beat the deadlines to a pulp, but rather to meet the deadlines with the best work product possible within the time permitted.

For bankers working on the commitment letter, a number of open conditions may initially exist on the commitment letter and the banker should work with the client to try to eliminate as many open conditions as possible prior to the Commitment Date. For example, if a banker states that Sally Streetwise’s parents must provide a “gift letter” for funds that were given to her to purchase her first home, it would be best to obtain the gift letter and have that condition cleared from the commitment letter, rather than having the commitment letter issued with the open condition. What if Sally’s parents refuse to sign a “gift letter” for the funds they provided her? These types of potential issues would be better discovered while in the contingency period rather than after the contingency has lapsed.

It is also critical to have an experienced banker who is familiar with the interplay of the Commitment Date and the board package timeframes. Less experienced bankers may issue a commitment letter quickly in an apparent effort to impress the borrower, but inadvertently trigger the 3-day deadline described above when the borrower is not yet ready to submit the board package.

With respect to the board package, Sally Streetwise will want to have an open dialogue with both her banker and her broker, so that they take the time to prepare a board package that shows Sally in the best light and is most likely to result in board approval. Sometimes this means waiting until the most recent bank statements are available from the buyer’s bank, or waiting until the perfect source of a professional reference is back from vacation.

There is one notable exception to the above. What should Sally do when she obtains a commitment letter that is still subject to a satisfactory appraisal, but the appraisal has not yet been conducted or approved by the bank? In such a case, the typical real estate contract states that a commitment letter subject to an appraisal is not a “Commitment Letter” as defined in the contract unless and until the appraisal condition is satisfied. The first goal would be to make sure the appraisal is satisfied before sending the Commitment Letter as part of the board package. However, there are times that the broker will want to submit the board package quickly, for example to make the next board meeting deadline, and so they would prefer to submit the commitment letter with the appraisal condition. In such a case, the buyer may decide to submit the commitment letter even though it is still subject to an appraisal, but the buyer should state that it is a preliminary commitment letter with their right to cancel still intact under the standard commitment letter contingency clause.

One final note on deadline extensions: buyers should take note that in the world of contract law, there is a difference between a deadline where a buyer is given a right of action and a deadline where a buyer has no such right. For example, take the case where a buyer with a finance contingency has done her best to cooperate with the bank to obtain a commitment letter, but through no fault of her own, the bank is unable to issue the commitment letter prior to the typical thirty-day deadline. In such a case, the buyer would potentially have the right to cancel the contract. Given that right, there is a possibility that a buyer could request from the seller an extension of that deadline rather exercising the right of cancellation. This wielding of the implied power to cancel often results in the seller granting an extension.

Contrast this situation with the deadline to submit a board package. Here, in the normal circumstance, the buyer does not have a right to cancel if the board package is not submitted on time, and therefore may not be successful in seeking an extension of such a time. Seeking an extension in such a circumstance comes with risk. If the seller does not agree (and there is no requirement that they do) then the buyer must rush to submit the board package or risk being held in breach of the contract, which potentially subjects the buyer to the loss of the deposit. If a broker or client is concerned with the board package submission deadline, the most effective time to address this concern is during the contract negotiation stage, when additional time can be added to the contract.

Due to the complex interplay of deadlines described herein, it is imperative that a buyer work with seasoned professionals when selecting a lawyer, broker, and banker. Each of these professionals works with the others to ensure that the deadlines are effectively met and with information that puts the buyer in the best possible position to succeed in the transaction.

PLEASE NOTE: This article is intended for informational purposes only and does not constitute the dissemination of legal advice. The deadlines and some of the legal language discussed herein is subject to negotiation between the parties involved and/or interpretation by a court of law. We encourage you to speak with the attorney handling your specific transaction for further details.

Cutting Through the Smoke: Applying Local Laws 141 & 147 to Cooperatives and Condominiums in New York City

As public opinion has turned against smoking, NY laws have followed. Smoking bans in public spaces have included stores, schools, and taxis in 1990, bans in restaurants and indoor bars in 2002, and parks, beaches, and pedestrian plazas in 2011. The popularity of the smoking bans in our public spaces have let legislative sights turn to residential buildings. The latest is Local Law 147 (“LL147”). Effective on August 28, 2018, LL147 requires residential buildings with three or more units to develop and distribute a written smoking policy. However, unlike the smoking bans, LL147 does not require condominium or cooperative boards to ban smoking in its entirety. Instead, it forces boards and unit owners to have a hard conversation and clarify what neighbors expect of each other. On its face, LL147 is agnostic about the content of the new smoking policies; it only asks that clear building policies are being put in place.

Even the laxest smoking policies distributed under LL147 may still be subject to other smoking laws targeting residential buildings, like Local Law 141 (“LL141”) which prohibits smoking or using electronic cigarettes in the common areas of most residential buildings. LL147 can make LL141 more transparent for residents by clearly outlining a smoking prohibition in the shared common areas while clarifying how the building will treat limited common elements like personal balconies and any other outdoor areas that may be connected to residential units.

On the other hand, for buildings looking to adopt a stricter policy, LL147 leaves open the door for boards to discuss and mandate a completely smoke-free environment throughout the building – including within individual apartments. If a board decides to go completely smoke-free, and adopts a new policy using the proper governing mechanisms, all residents may be required to follow the policy, including unit owners, their future renters (current renters may be carved out depending on their leases), and anyone invited onto the premises. Because LL147 leaves it to the buildings to self-govern, it sidesteps the issue of whether the law allows for strict regulations that pierce the sanctity of the home. Even buildings whose residents largely support going smoke-free may still be cautious about how a strict ban can be properly applied, implemented, and enforced.

Like pet policies, smoking policies can feel very personal. For prospective purchasers sensitive to smoke or those who are avid smokers, reviewing the new smoking policy is another important item to flag for your brokers and attorneys during the diligence phase of vetting a new home. But for unit owners caught off guard by a new strict policy or prospective buyers who don’t like what the diligence reveals, know that ultimately any policy is subject to change; it comes down to what your board and your neighbors want. Ultimately LL147 is just a harbinger – potentially showing a trend towards stricter smoking regulations to come.

5 Things to Consider When Choosing a NYC Real Estate Attorney

When buying or selling a property, a knowledgeable lawyer that practices Real Estate law will help make sure you get exactly what you want out of the transaction.

1. Knowledge of New York City Residential Transactions

The “Concrete Jungle” has a unique housing stock unlike anywhere else in the U.S. For example, the great majority of Co-ops that exist in the U.S. are in New York City. Because of these unique features, there are intricacies to closing a NYC Real Estate Transaction that a well-qualified attorney can help to explain. These include things like knowledge of local regulations, understanding the custom and practices in cooperative, condominium and house purchases, experience dealing with the New York City network of brokers. Additionally, it is preferable to have an attorney who has completed sales in the building, or similar buildings, that you plan to buy/sell in. Knowledge in the field means knowing what to look for to ensure the transaction goes as smoothly as possible.

2. Personalized Attention

You do not want a Real Estate Attorney who takes a cookie cutter approach to one of the most important transactions of your life. A good real estate attorney will give you personalized attention and be available to answer the questions you have when they come up. To achieve this, it is important to have a team of individuals working on your transaction, rather than just one person. Extra sets of eyes ensure that details are not overlooked.

Also, you want to make sure that an attorney is working on your transaction, not just a paralegal or an administrative assistant. Some firms assign only a paralegal to the transaction, a practice we do not employ. Many times we have two attorneys working on one transaction, both for a smooth client experience and to allocate resources where they are most needed.

Like a doctor with good bedside manner, a good attorney will form a close bond with their client that is based on mutual respect and trust. Despite all the lawyer jokes you may have heard, most attorneys are hard-working, excellence driven, respectful individuals who are trying to do their best for their clients. Our firm puts a focus on this aspect of the relationship because we feel it is the centerpiece of the real estate transaction puzzle.

3. Fees

Fees will vary depending on the size and complexity of a transaction. They will generally be structured as a flat fee, with half payable up front and the balance payable after closing. Factors that affect the fee, include but are not limited to: (1) whether the purchase will be made in cash or require a mortgage; (2) if there is a lender, whether it is an institutional or a private lender; (3) whether the transaction involves Federal or State tax withholdings; (4) whether the client will be able to attend the closing; (5) whether there are any anticipated title issues; (6) whether the transaction includes anything that is not part of the normal process of buying or selling a property in NYC.

Some firms will refer to all or a portion of the fee as “non-refundable.” We do not agree with this approach and will refund any unused portion of the retainer on any transaction. Other firms will say “no fee if we do not get you to the closing.” We do not agree with this approach either, as we feel it will create a conflict of interest where the attorney may unconsciously rush to conclude a transaction or hold back emphasis on any issues that arise that might jeopardize the transaction in any way.

See an article on the firm’s origin and philosophy here.

4. Provide Consultation and Guidance on all Aspects of the Transactions

A good real estate attorney will advise you on all of the risks associated with the transaction and guide you on how to proceed. They will advise you, not only on the legal aspects of the transaction, but also help you to identify and manage the wide assortment of risks that affect the viability of a residential transaction. This includes reviewing board minutes, building financials, the offering plan, and other important documents. In addition, an attorney will help you coordinate a loan commitment, negotiate a contract for a sale and much more.

A good attorney will also know how to allow a client to be a valuable resource as well. Even if a client knows nothing about real estate or financing, they can still provide key information about the condition of the property, what it looks like, what they expect to receive, and what their most important needs are from the property. A good attorney will know when to ask questions and when to provide answers, while a not-so-good attorney thinks they know all the answers and never asks a single question.

5. Team Player with Proven Track Record

It is important to choose an attorney who is empathetic to your needs, works well with others, and has a proven track record supported by professional referrals. Ultimately, choosing an attorney is a very personal process. Check out information on our firm here!

NYC Real Estate Attorney’s Closing Report: June 2018

Just a few of our recent closings. If you are also looking to buy or sell at these property addresses, you might want to give us a call.

| Property | Value | Transaction |

| 1060 Park Avenue, NY, NY | $1,317,500 | Coop Purchase |

| 300 West 135th Street, NY, NY | $1,040,000 | Condo Purchase |

| 420 East 51st Street, NY, NY | $645,000 | Coop Sale |

| 401 East 86th Street, NY, NY | $1,349,000 | Coop Purchase |

| 525 East 86th Street, NY, NY | $825,000 | Coop Sale |

| 170 John Street, NY, NY | $2,300,000 | Condo Sale |

| 132 East 35th Street, NY, NY | $865,000 | Coop Sale |

| 561 41st Street, BK, NY | $582,500 | Coop Purchase |

| 680 West 204th Street, NY, NY | $380,000 | Coop Purchase |

| 1199 Park Avenue, NY, NY | $3,325,000 | Coop Purchase |